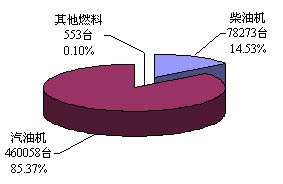

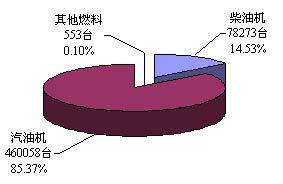

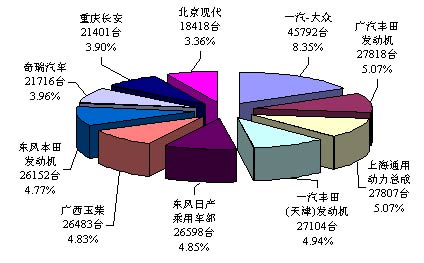

First, the overall situation According to the latest statistics from the China Association of Automobile Manufacturers, a total of 538,884 engines were produced in November, a decrease of 7.42% from the previous period; sales of engines were 548,640 units, a year-on-year decrease of 13.24%; production of motor vehicles was 685,996 units, a decrease of 2.68%; sales of motor vehicles were 685,154 units, a decrease of 4.26 %. From January to November of 2008, a total of 7,918,690 engines were produced, a cumulative increase of 7.00% over the same period; sales of engines were 8,023,602 units, a cumulative increase of 8.89% over the same period; domestic engine market entered a year-on-year negative growth for the first time since August, despite the emergence in September. After the miraculous turnaround, due to the spread of the international financial crisis and the impact of the economy, the engine market was once again affected. The engine market has entered the “two consecutive shades†for two consecutive months. This shows that the overall engine market is in a weak position. Still did not really look up. Until November, when the output and sales of the engine market were both lower than 600,000 units, it seems that the increase in the total production and sales volume of the engine in 2008 will fall below the double digits for the first time in recent years. Second, according to the fuel classification of engine production and sales 1. The composition of each fuel engine output Table 1 Production of Engine Sub-models in November 2008 Table Unit: Taiwan, % In November 2008, the growth trend of the market demand for diesel engines and gasoline engines compared with October was not stable, and only gasoline engines showed a growth trend. A total of 78,273 diesel engines were produced in November, a 35.57% decrease from the previous month. This is the second time that the number of diesel engines dropped by less than 30% since 2008; gasoline engine 460058 units, an increase of 0.01% over the previous period; and 553 other fuel engines, a decrease of 3.66%; In November, the proportion of production of each product was higher or lower than that in October: Diesel -6.34% and Gasoline Engine 6.34%. Figure 1 Composition of engine output for November 2008 2. Composition of sales of each fuel engine Table 2 Sales of Engine Sub-models in November 2008 Table Unit: Taiwan, % In November 2008, the market demand for diesel engines and gasoline engines showed a downward trend compared with October. Only other fuel engines showed a growth trend. In November, a total of 97,973 diesel engines were sold, a decrease of 25.92% compared with the previous month; 450,129 gasoline engines were sold, a decrease of 9.91% compared to the previous period; The number of fuel engines was 538, an increase of 9.35% compared with the previous month. In November, the proportion of sales volume of each product sold was increased or decreased compared with that of October: diesel engine -3.05%, gasoline engine 3.03%, and other fuels 0.02%. Figure 2 Composition of Engine Sales in November 2008 [next] Third, according to the company ranking engine sales and market share Table 3 Top 10 Engine Companies in November 2008 Table Unit: Taiwan, % In November 2008, after several months of negative growth in the engine market, in the “Jin 9 Silver 10â€, the engine market saw a growth rate of 26% in September, but in October and November Back to the negative growth of the previous months. According to the latest statistics from the China Association of Automobile Manufacturers, in November 2008, the growth trend of the top 10 engine companies was not stable. Among them: FAW-Volkswagen (45,792 units), an increase of 17.39%; GAC Toyota Motor (27818 units), an increase of 0.24%; Shanghai General Powertrain (27,807 units), an increase of 52.64%; Dongfeng Nissan Passenger Vehicles Co., Ltd. ( 26,598 units), an increase of 24.08% from the previous period; Chery Auto (21716 units), an increase of 7.22% from the previous period. All five engine companies have shown a different degree of growth; while FAW-Volkswagen took the lead in November with 45,792 units. This is Since 2008, FAW-Volkswagen has led engine companies for the second time; FAW Toyota (Tianjin) engines (27,104) have fallen by 2.74%, and Guangxi Yuchai Machinery (26,483) has dropped by 10.48% from the previous month; Dongfeng Honda Engine ( 26152 units), a decrease of 7.06 percent from the previous period; Chongqing Changan Automobile Co., Ltd. (21,401 units), a decrease of 20.87% from the previous period; Beijing Hyundai Motor (18418 units), a decrease of 5.39% from the previous period. All five companies have experienced declines in various degrees. In contrast, Liuzhou Wuling Liugong Power, which took the lead in October last month, has not entered the top 10 in this month and the four companies of Shanghai Volkswagen, Harbin Dongan Automobile Engine and China FAW Group have not entered the top 10. Homes were replaced by Shanghai Powertrain, Dongfeng Nissan Passenger Vehicles, Chery Automobile and Beijing Hyundai. Shanghai GM Powertrain ranked the third with a 52% growth rate. The top 10 engine companies sold a total of 269,289 engines, which accounted for 49.08% of the total sales of engine companies in November 2008. Figure 3 Top 10 engine sales companies in November 2008 and market share IV. Top 10 Sales by Chai Gasoline Engine Group 1. The sales of the top 11 diesel engine companies Table 4 Top 10 Sales of Diesel Engines in November 2008 Table Unit: Taiwan, % In November 2008, the total sales volume of diesel engine enterprises was 97,973 units, a decrease of 25.92% from the previous quarter. In November, the total sales of the top 10 diesel engine manufacturers fell by 26.43%. Compared with October, only one company with a positive growth from the previous quarter was Qingling Motors (Group) (2,975 units), an increase of 31.12% compared to the previous period; although Qingling Motors (Group) ranked eighth, the company is The only company in the top 10 rankings was positive growth in November; the remaining nine companies all experienced different degrees of decline; among them: Guangxi Yuchai Machinery Group (26,483 units), a decrease of 10.48%; China First Automobile Group (13742 units) ), 44.40% MoM, Kunming Yunnei Power (10478), down 16.74% MoM; Dongfeng Chaoyang Diesel Engine (8894), a 31.58% decrease from the previous quarter; Weichai Holdings (6359 units), a decrease of 34.09% MoM; Dongfeng Motor Shares of 5,492 units fell 36.83% compared to the previous period; Jiangxi Jiangling Motors Holdings (5,256 units) decreased 17.77% month-on-month; Yangzhou diesel (4443 units) dropped 22.05%, and China Heavy-duty Truck Group (2766 units) fell 49.85% from the previous period; and Compared with last month, although Guangxi Yuchai Machinery Group is still in a downward trend, the decline in floating has rebounded from last month, and it continues to top the list for the month. This is the first consecutive month since Guangxi entered into the Yuchai Machinery Group in 2008. champion. In contrast, the five companies of China First Automobile Group, Dongfeng Chaoyang Diesel Engine, Weichai Holdings Group, Dongfeng Motor Co., Ltd. and China National Heavy-duty Truck Group slipped more than 30% to 40% respectively this month. The total sales volume of the top 10 diesel engine companies was 86,888 units, accounting for 88.69% of the total sales of the top 10 diesel engine companies in November 2008. Figure 4 The top 11 diesel engine manufacturers in November 2008 compared with October 2. Top 10 Sales of Gasoline Engine Engines Table 5 Top 10 Gasoline Engine Sales in November 2008 Table Unit: Taiwan, % New Co2 laser engraving and cutting machine. The machine is a kind of Laser Engraving Machine System equipped with CO2 laser Tube, it is used to engrave on wood, bamboo, plexiglass, crystal, leather, rubber, marble, ceramics and glass and etc. It is most suitable and the preferred choice of equipments in industries such as advertisement, gifts, shoes,toys and etc. It supports multiple graphic formats, such as HPGL, BMP, GIF, JPG, JPEG, DXF, DST, AI and so on.

This machine is equipped with DSP Control System for RDdraw directly,also supports CoreDraw and Auto CAD and other advance software. It must connect with computer with USB cable when you change the settings of machine for the design files,you can transfer the file with USB memory stick to the machine, or can download it to the machine directly with USB cable from computer. Even on the same Job, you can do setting with different colour in the software and also can making holes.And it can the legs separate from the main body of the machine. The machine has doors which can be opened to accommodate larger materials.

It adopts self-developed Co2 laser and has strong cutting ability and efficiency. It integrates laser cutting, It is a high-end high-tech Co2 laser cutting machine integrating advanced technologies such as precision machinery and numerical control technology.

CNC Co2 laser cutting machine is the first choice in the non-metal material processing industry, with strong cutting ability "General" cutting speed, ultra-high stability, high-quality processing, extremely low operating cost and ultra-high adaptability.

Hot sale CO2 laser machine,Co2 Laser Cutting Engraving Machine,Mini 50W Co2 Laser Engraving Machine,Wood Laser Engraving Machine Zhongcan Technology Co.,Ltd , https://www.zhongcanlaser.com Engine classification Completed in November Completed in October Moment growth Proportion of production in November 2008 Proportion of production in October 2008 Increase in proportion of output Total engine 538884 582090 -7.42 100 100 - diesel engine 78273 121493 -35.57 14.53 20.87 -6.34 gasoline engine 460058 460023 0.01 85.37 79.03 6.34 Other fuels 553 574 -3.66 0.1 0.1 0

Engine classification Completed in November Completed in October Moment growth November 2008 share of sales Proportion of sales in 2008 Increased proportion of sales Total engine 548640 632369 -13.24 100 100 - diesel engine 97973 132247 -25.92 17.86 20.91 -3.05 gasoline engine 450129 499630 -9.91 82.04 79.01 3.03 Other fuels 538 492 9.35 0.1 0.08 0.02

Rank Company Name Sales volume Moment growth market share 1 FAW-VW Automotive Co., Ltd. 45792 17.39 8.35 2 Guangzhou Automobile Toyota Engine Co., Ltd. 27818 0.24 5.07 3 Shanghai General Powertrain Co., Ltd. 27807 52.64 5.07 4 FAW Toyota (Tianjin) Engine Co., Ltd. 27104 -2.74 4.94 5 Dongfeng Nissan Passenger Vehicle Division 26598 24.08 4.85 6 Guangxi Yuchai Machinery Group Co., Ltd. 26483 -10.48 4.83 7 Dongfeng Honda Engine Co., Ltd. 26152 -7.06 4.77 8 Chery Automobile Co., Ltd. 21716 7.22 3.96 9 Chongqing Changan Automobile Co., Ltd. 21401 -20.87 3.9 10 Beijing Hyundai Motor Company Limited 18418 -5.39 3.36 Top 10 Total 269289 4.06 49.08

Rank Company Name Sales volume Moment growth market share 1 Guangxi Yuchai Machinery Group Co., Ltd. 26483 -10.48 27.03 2 China First Automobile Group Corporation 13742 -44.4 14.03 3 Kunming Yunnei Power Co., Ltd. 10478 -16.74 10.69 4 Dongfeng Chaoyang Diesel Engine Company 8894 -31.58 9.08 5 Weichai Holding Group Co., Ltd. 6359 -34.09 6.49 6 Dongfeng Motor Co., Ltd. 5492 -36.83 5.61 7 Jiangxi Jiangling Motors Holding Co., Ltd. 5256 -17.77 5.36 8 Yangzhou Diesel Engine Co., Ltd. 4443 -22.05 4.53 9 Qingling Automobile (Group) Co., Ltd. 2975 31.12 3.04 10 China Heavy Vehicle Group Corporation 2766 -49.85 2.82 Top 10 Total 86888 -26.43 88.69

Rank Company Name Sales volume Moment growth market share 1 FAW-VW Automotive Co., Ltd. 44801 17.57 9.95 2 Guangzhou Automobile Toyota Engine Co., Ltd. 27818 0.24 6.18 3 Shanghai General Powertrain Co., Ltd. 27807 52.64 6.18 4 FAW Toyota (Tianjin) Engine Co., Ltd. 27104 -2.74 6.02 5 Dongfeng Nissan Passenger Vehicle Division 26598 24.08 5.91 6 Dongfeng Honda Engine Co., Ltd. 26152 Hot sale CO2 laser machine